15-Minute Guide to Retirement Planning

Written by: Chuck Mattiucci, AIF® | Financial Advisor

You may love your career and find your work fulfilling, but you likely don’t plan on working for the rest of your life. If you hope to retire at some point, you need to have a plan and money set aside. Retirement planning is an active process, something you need to be involved in from day one. Whether you’ve just started your first job or have been in the workforce for some time, it’s never too early or too late to start planning for what comes next.

Consider this your quick-start retirement planning guide to get and keep yourself on track, no matter where you are in your career.

What Is Retirement Planning?

Retirement is what comes after years of working or following a career path. The average person spends about 20 years in retirement according to the U.S. Department of Labor, although there’s some variation. That means the average person should have enough savings to support themselves for about 20 years without working. Another term for retirement is financial independence, meaning you have enough invested or saved to live as you want, without having to work.

A retirement plan is designed to make sure that you have the financial resources available to support yourself and maintain your lifestyle once you leave the workforce. Retirement planning is a multistep process. First, you need to figure out how much you’ll need to save to retire comfortably and maintain your standard of living. Next, you’ll need to consider what you want your life to look like after retirement. From there, you can focus on how to save and invest your money.

Several factors influence your overall approach to retirement planning. Your age is one factor — younger people often save less but have more opportunity for their savings and investments to grow thanks to a longer time horizon. Your risk tolerance is another factor. If you’re nearer to retirement, you might have a lower risk tolerance than a person who is just getting started and has decades to let their investments grow.

The options available to you also influence your overall retirement plan. You might work for a company that sponsors a retirement plan, such as a 401(k). Alternatively, you might be self-employed and need to explore other options. A financial advisor who’s a fiduciary can help you put together a plan to meet your retirement goals and live a comfortable life after you’ve stopped working.

How to Start the Retirement Planning Process

With so many options at your disposal, you’re never too young or too old to begin planning for retirement. The first step of retirement planning should come from within. Take some time to envision your ideal retirement. How old would you like to be when you retire? How much would you like to have saved up? Goal visualization can help to inform your ultimate strategy.

You’ll want to begin saving and investing with some goals in mind. Calculate your income, establish a budget, then either set up automatic transfers into an investment account or plan time to do so manually. Your retirement strategy should also include and prioritize prompt debt elimination.

Many companies offer compensation packages, like 401(k) or 403(b) plans that pay out matching contributions from the employee and employer at the time of retirement. Other viable retirement plan options include mutual funds and exchange-traded funds (ETFs) that spread your investment across a wide range of securities.

Another option worth considering is partnering with a financial advisor. The right advisor can offer numerous financial services that can help individuals retire with confidence.

15-Minute Guide to Retirement Planning

Even if retirement seems far away or too big to think about today, your future self will be grateful for taking the time to map out a plan and get the wheels turning. It only takes 15 minutes or so to get the ball rolling on retirement. Here’s what you can do.

1. Know When to Start Planning for Retirement

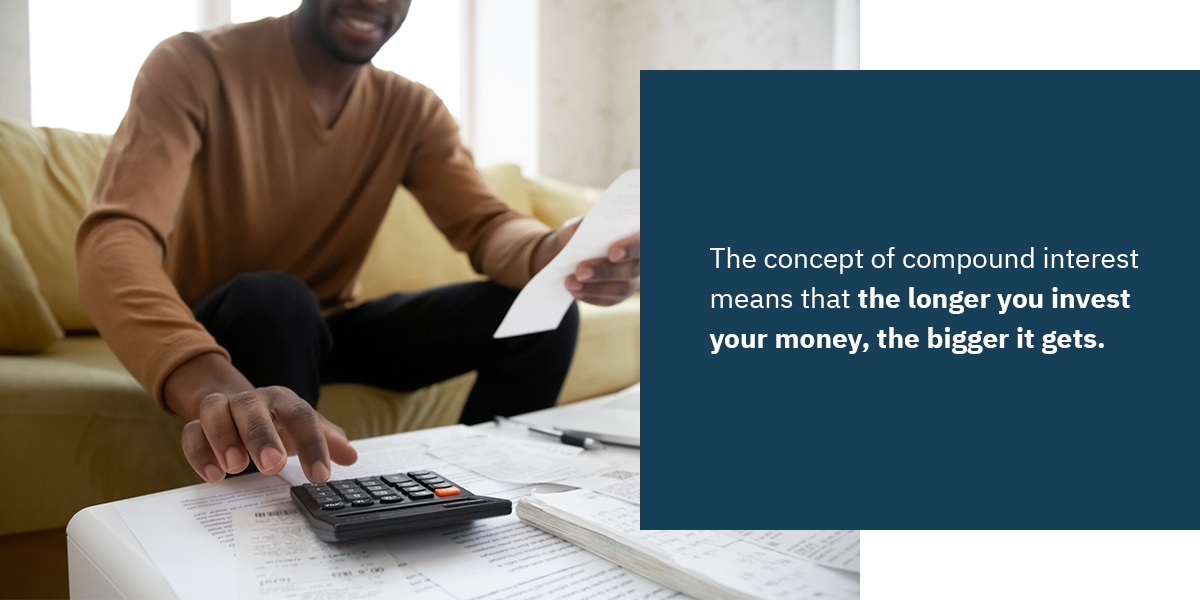

The best time to start planning for retirement is right away. Ideally, you’ll start saving and investing for retirement when you get your first job. The earlier you start setting money aside for the future, the more time that money has to grow and build wealth for you. The concept of compound interest means that the longer you invest your money, the bigger it will get. With compound interest, the money your investment earns gets added to the initial amount, increasing the amount of interest the investment earns.

For example, if you invest $5,000 at age 20 and let it sit for 45 years with a 5% interest rate, you’ll have $44,925.04 if you retire at age 65 — even if you don’t add to the initial $5,000 investment. If you wait until age 35 to invest $5,000 and let it sit for 30 years while earning a 5% rate of return, you’ll have just $21,609.71.

While it’s ideal to start early when it comes to making a retirement plan, it’s also never too late to get started. If you’re in your 30s, 40s, or 50s, you can still begin making a plan. At this stage in life, you might have more to invest than you did in your 20s, which can help make up for some lost time.

2. Know How to Set Your Retirement Goals

Once you’ve committed to saving for retirement, the next thing to do is consider how much you’ll need to save by the time you hit retirement age. Having a somewhat concrete number to work toward can help you see if you’re on track as the years go on.

There are a few things to consider when setting a goal for retirement:

- Your age: How old you are today influences how long you have until you retire and how much you need to save each month to reach your target. The younger you are, the less you need to set aside, as your savings will have more time to grow. You can use a retirement savings calculator to figure out how much you’ll end up with in retirement based on what you save and your current age.

- Your lifestyle: The typical recommendation is to have between 70% and 90% of your income before retirement saved for each year you plan on being retired. How you plan on living once you’ve retired influences the amount of annual income you’ll need. If you expect to travel a lot or live lavishly, you’ll likely need more saved than someone who expects to downsize or live more modestly. Other factors, such as your health, can also affect your costs in retirement.

- Your expected longevity: Life expectancy in the U.S. is 78.7 years, but you may live for much longer once you leave the workforce. When considering how much you’ll need to save for retirement, it can be helpful to assume you’ll live for at least 20 years after retiring.

3. Know How to Assess Your Risk Tolerance and Review Investment Strategies

One piece of advice people often get about retirement planning is not to focus too much on the small details. The market will go up and down over the years. For the sake of your nest egg, it’s important not to panic every time your investments take a dip. However, it’s good to have an idea of your overall risk tolerance and to work with an advisor to develop an investment strategy that works for you.

Risk tolerance is the amount of risk you can stand. When it comes to investing, it’s often true that the riskiest investments can have the biggest rewards. The trade-off is that you could lose a lot of money if things don’t pan out. People often have more risk tolerance when they are younger, and retirement is still decades in the future. As you get nearer to retirement age, your risk tolerance is likely to drop, and you’re more likely to choose more conservative investments. The investments might have a lower rate of return compared to riskier options, but there’s also a lower risk that you’ll lose a considerable sum.

You might need to adjust your investment strategy as the market fluctuates and your needs change. For example, as you get nearer to retirement, your financial advisor might recommend moving some of your portfolio to more conservative investments to help reduce risk.

A financial advisor can help you calculate your risk tolerance and make investment recommendations accordingly. When you work with a fiduciary, you’re working with someone who has a legal responsibility to recommend investments that are in your best interest, meaning they can’t recommend an investment that would benefit them more than you.

4. Know What to Include in Your Retirement Plan

Depending on where you work and how much you earn, you might have several options when developing a retirement plan or deciding where to put your retirement savings. The more comprehensive and well-rounded your retirement plan is, the better. You want a plan that helps you minimize your tax burden while maximizing the potential for return. Here’s what to think about when deciding where to put your money:

- Retirement account options: Many employers offer 401(k) plans or similar, which allow you to set aside pretax money for retirement. If you’re under age 50, you can invest up to $19,500 per year in an employer-sponsored plan. Depending on your income, you can also save up to $6,000 per yearin an IRA. An IRA can be an option even if you don’t have a plan through an employer. If you’d like to save more than the limits on either a 401(k) or IRA, you can set money aside in an individual investment account.

- Social Security: Many people in the U.S. will qualify for Social Security benefits once they reach retirement age. While your Social Security benefits aren’t likely enough to support you in retirement fully, they can supplement your retirement income.

- Life insurance: While life insurance shouldn’t be your sole source of retirement income, some people decide to use it as a supplement to their other investments. A permanent life insurance policy might offer a cash value component, which can provide additional income once you retire. Since permanent life insurance policies tend to cost much more than term life insurance and because the returns on a cash value plan might not be substantial, it’s a good idea to discuss the benefits of incorporating life insurance into your retirement plan with a fiduciary advisor.

- Estate planning: You may be thinking of the future of your heirs when you develop a retirement plan. Estate planning can be part of retirement planning. It can make sense to consider your legacy and how to minimize the tax burden on your heirs when you develop a retirement strategy.

Behavioral Finance Tips

It can be easy to let your emotions get the better of you when it comes to financial planning and saving for the future. Uncertainty is part of life and can be tough to deal with occasionally. To keep your retirement on track and avoid veering off course, it helps to keep a few things in mind:

- See the big picture, but focus on the here-and-now: You’ve probably heard that you need to save $1 million or more to have a comfortable retirement. While that might be true, don’t let concerns about the “big number” keep you from making steady progress on your goal. Save as much of your income as possible and start saving as early as possible to make it more likely you’ll have enough to live on in retirement. Remember, you can always adjust your goals as your financial situation changes.

- Automate the process: The less you have to think about saving for retirement, the more likely you’ll be to do it. When and where you can, automate your savings. That can mean asking your employer to automatically send 10% of your paycheck to your 401(k) or setting up recurring transfers from your checking account to an IRA.

- Remember, slow and steady wins the race: Trends and fads will come and go with time. It can be easy to get wrapped up in the next big thing and tempting to chase investments that look particularly promising. Since trendy investments can also be the highest risk, it’s often better to avoid chasing them and stick with the tried and true.

- Check-in regularly with a financial advisor: You don’t have to go it alone with retirement planning. A financial advisor can guide you, making recommendations that are in your best interests. Schedule regular check-ins with an advisor to make sure you’re on track and adjust your plan as your needs and situation change.

Retirement Planning FAQ

No matter where you are in the retirement planning process, you’re likely to have a few questions about how it works and what you can expect. Check out some answers to the most commonly asked questions:

What Are the Steps in Retirement Planning?

Retirement planning includes setting a goal, prioritizing your goals, deciding where to save your money, and choosing the right investments for you.

What Does a Retirement Planner Do?

A retirement planner works with you, taking your current situation and financial goals into account, to help you put together a plan that will get you on track and help you achieve your goals.

Should I Start Working With a Retirement Planner?

If you aren’t sure how to save for retirement or where to invest your money, it’s a good idea to work with a financial advisor. Even if you schedule a single meeting with an advisor, working with one can help jumpstart your retirement savings and set you up for a more secure financial future.

What Questions Should I Ask My current Retirement Planner?

There are a lot of questions you can ask a retirement planner to help make sure they’re a good fit for you and that they’ll do what it takes to help improve your financial situation. Ask them how they are compensated, how they make recommendations, and how much experience they have in financial planning.

What Is Risk Tolerance?

It’s important to recognize that any investment comes with a certain amount of risk. Even the most stable investments leave your money to chance. Risk tolerance describes how much risk you’re willing to accept in an investment.

How Much Should You Save for Retirement?

When you retire, all of your income will come from Social Security, your investment strategy, and the amount you saved while working. Your investment and Social Security income should replace at least 70%-90% of what you make while employed to continue your lifestyle as usual. Budgeting 10%-15% of your pre-tax income will help ensure your investment meets your needs during retirement.

What Age Do Most People Retire?

According to Annuity.org’s research, the current average age for retirement is 62. The retirement age rises to 64 for employees currently working. Waiting to retire will give you more time to save, but retiring earlier gives you more time to experience the benefits.

Talk to an Advisor About Retirement Planning Today

When choosing a financial advisor to help you put together a retirement plan, look for a company that has a fiduciary duty to you. Advisors aren’t salespeople but are fiduciaries and have a legal duty to look out for their client’s best interests, not their own bottom line.

Fort Pitt Capital Group’s Registered Investment Advisors are available to help you develop a plan for the future, including retirement. Contact us today to discuss your investment goals and start making a plan for your financial future.

Chuck Mattiucci, AIF®

Senior Vice President

Fort Pitt Capital Group, LLC

680 Andersen Drive, Pittsburgh, PA 15220

(412) 921-1822 | cmattiucci@fortpittcapital.com

Fort Pitt Capital Group is an investment advisor registered with the United States Securities and Exchange Commission (“SEC”). For a detailed discussion of Fort Pitt and its investment advisory fees see the firm’s Form ADV Part 1 and 2A on file with the SEC at www.adviserinfo.sec.gov.